WhatsApp Based Bookkeeping App - A Design and Business Viability Validation Study

This is a design and business viability validation study that will take you through the complete end-to-end process of validating a product's business viability. This study helps you build a business model that is genuinely sustainable in the long run.

5/5/20267 min read

This article is going to be presented in an academic paper format to help you understand the complete technicality that goes into validating the business viability of a product.

A Conversational Bookkeeping Assistant for Small Service Businesses: A Design and Business Viability Validation Study

Abstract

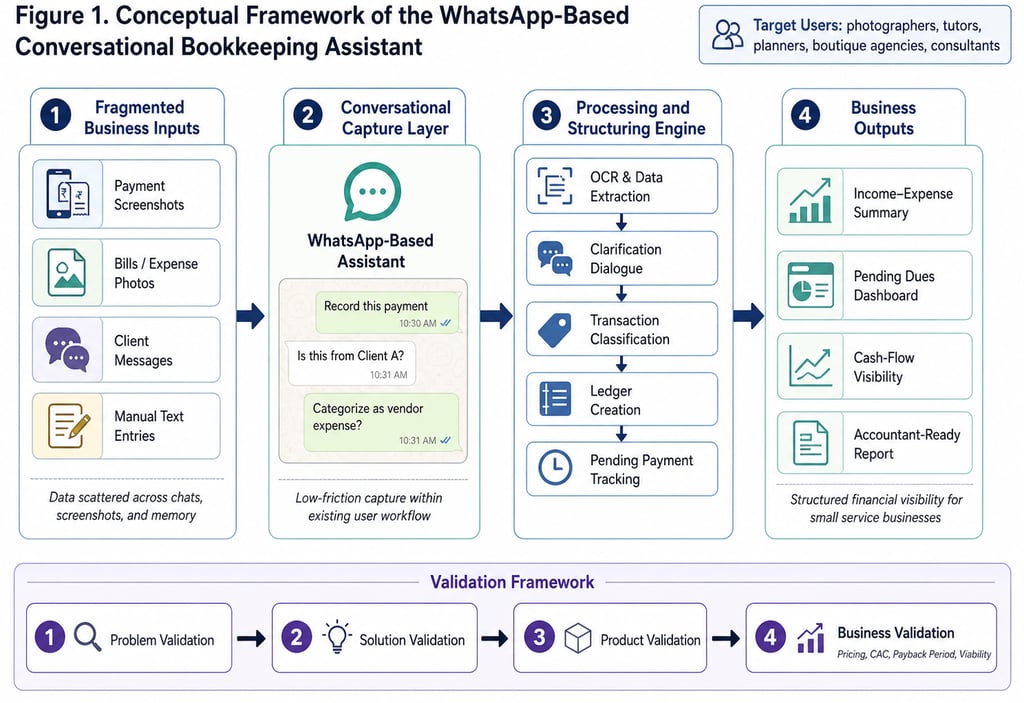

Small service businesses often conduct client communication, payment follow-ups, expense sharing, and informal record-keeping through messaging platforms, while their formal bookkeeping remains scattered across payment applications, screenshots, notebooks, spreadsheets, and accountant-led month-end consolidation. This creates a practical gap between daily business activity and structured financial visibility. This paper proposes a WhatsApp-based conversational bookkeeping assistant designed for small service businesses such as freelancers, boutique agencies, tutors, event planners, photographers, decorators, and local service providers. The proposed system allows users to forward payment screenshots, bills, invoice requests, expense images, and client messages to a conversational assistant, which then classifies transactions, tracks pending payments, creates monthly summaries, and prepares accountant-ready reports. The paper studies the problem through the lens of digital payment growth, small business accounting challenges, conversational interface adoption, and business viability. It also presents a scenario-based business validation model using customer acquisition cost, average revenue per account, gross margin, payback period, and pricing sensitivity. The study argues that while the product may appear attractive as a low-cost bookkeeping tool for individual users, its stronger business potential lies in positioning it as a cash-flow visibility and payment control tool for small service businesses. The paper concludes with a proposed validation methodology for future empirical testing through prototype deployment, user interviews, feature adoption tracking, and willingness-to-pay analysis.

Keywords: conversational bookkeeping, small business accounting, WhatsApp Business, MSME digitization, financial technology, business validation, customer acquisition cost, SaaS feasibility

1. Introduction

Small businesses rarely suffer from the absence of business activity. More often, they suffer from the absence of structured visibility around that activity. A tutor may receive fees through UPI, confirm classes through WhatsApp, maintain student names in a notebook, and send monthly details to an accountant through screenshots. A wedding photographer may discuss packages with clients on WhatsApp, receive partial payments through QR codes, pay vendors in cash or UPI, and later struggle to remember which payment belonged to which project. A boutique agency may manage multiple clients, invoices, advances, reimbursements, and vendor bills without a dedicated finance team.

This is not a technology-availability problem alone. India has seen a rapid expansion of digital payments. UPI contributed around 80% of retail digital payments in India in FY 2023–24, with transaction volume exceeding 131 billion and transaction value crossing ₹200 lakh crore [1]. The MSME sector is also economically significant: official Indian government data states that MSMEs accounted for 30.1% of India’s GDP, 35.4% of manufacturing, and 45.73% of exports, while the Udyam portal had more than 3.80 crore units in its database as of 2025 [2].

Yet, the spread of digital payments does not automatically create disciplined bookkeeping. In many small businesses, the transaction may be digital, but the context around the transaction remains informal. A ₹15,000 UPI payment may arrive, but unless the owner records whether it belongs to a client advance, final payment, vendor settlement, reimbursement, or personal transfer, the digital trail alone does not create clean books.

The problem becomes more visible in service businesses because these businesses often operate through conversations rather than standardized point-of-sale systems. A large retail business may have billing software, inventory systems, and GST workflows. A small interior designer, tuition class, event planner, photographer, consultant, or repair-service owner may instead rely on WhatsApp chats, screenshots, voice notes, and memory. This creates a gap between how the business actually operates and how bookkeeping software expects the business to behave.

This paper proposes a conversational bookkeeping assistant that meets the user inside their existing workflow rather than forcing them to adopt a separate accounting system from the beginning. The proposed assistant is built around WhatsApp because messaging interfaces are familiar, low-friction, and already used by small businesses for communication. WhatsApp Business is positioned by Meta as a free-to-download app with built-in tools for businesses to build trust and manage conversations [3]. WhatsApp’s broader messaging platform is also widely used globally, with the official app listing describing it as being used by over two billion people across more than 180 countries [4].

The purpose of this paper is not only to propose the system but also to examine whether such a product can become a viable business. Many college project reports stop at technical feasibility: whether the system can be built. However, if the project is evaluated as a product idea, technical feasibility is only one part of validation. A useful product may still fail if customers are too price-sensitive, acquisition costs are too high, churn is too high, or the wrong buyer is targeted. Therefore, this paper includes a business validation framework in addition to the system design.

2. Problem Background

Small service businesses often face a specific bookkeeping problem: their financial data is not absent, but fragmented. Income may be visible in bank statements and UPI history. Client commitments may exist in WhatsApp conversations. Expenses may be present as vendor bills, screenshots, photos, or memory-based notes. Accountant communication may happen at the end of the month or financial year, when the owner is expected to reconstruct the business history from multiple sources.

This creates four operational issues.

First, owners lose real-time visibility of cash flow. They may know that sales are happening but may not clearly know how much money was collected, how much remains pending, and which vendors need to be paid.

Second, unpaid invoices and partial payments become difficult to track. Many small service businesses work with advance payments, milestone payments, and final settlements. Without structured tracking, the owner may have to manually search chat histories or payment screenshots.

Third, accountant dependency increases. Instead of sending organized records periodically, the business owner often sends scattered information at the last minute. This increases reconciliation effort and creates avoidable stress.

Fourth, existing accounting software may feel too formal or effort-heavy for early-stage or micro businesses. Studies on accounting software adoption in small businesses commonly examine factors such as perceived usefulness, perceived ease of use, organizational readiness, and the role of technology acceptance. For example, a 2022 study on accounting software acceptance among small businesses in India used survey data and structural equation modelling to understand adoption behaviour [5]. This supports the idea that adoption is not only a matter of software availability; it is also shaped by how easy and useful the system feels to the target user.

The proposed solution addresses this adoption gap by using a conversational interface. Instead of requiring the user to open an accounting application and manually enter every transaction, the user can forward business-related financial material to a WhatsApp assistant. The assistant then extracts, classifies, and organizes the data.

3. Business Validation Framework

A technically functional product is not necessarily a viable business. Therefore, this study includes a business validation framework.

The proposed business validation framework has four stages:

Problem validation

Solution validation

Product validation

Business validation

3.1 Problem Validation

The key problem hypothesis is:

Small service business owners struggle to maintain structured financial records because their business data is scattered across WhatsApp conversations, payment screenshots, bills, spreadsheets, and accountant communication.

Validation methods:

Semi-structured interviews with 25–40 small service business owners

Observation of current bookkeeping practices

Collection of pain-point frequency data

Identification of current tools used for payment tracking and accounting

Assessment of month-end and tax-season stress points

Sample interview questions:

How do you currently track client payments?

How do you remember pending payments?

How do you send information to your accountant?

How often do you update your financial records?

What happens when a payment screenshot is received?

Do you know your monthly income and expenses without asking your accountant?

3.2 Solution Validation

The key solution hypothesis is:

A WhatsApp-based assistant will reduce bookkeeping friction because users can record financial data through a familiar communication interface.

Validation methods:

Clickable prototype

Wizard-of-Oz simulation, where a human manually performs backend classification while the user experiences it as an assistant

User feedback on ease of use

Comparison with spreadsheet/manual methods

Willingness-to-pay questioning

Success indicators:

Users understand the concept without extensive training

Users prefer forwarding screenshots over manual data entry

Users trust the monthly summary after reviewing it

Users are willing to use the assistant at least weekly

3.3 Product Validation

The key product hypothesis is:

Users will repeatedly use the assistant to capture income, expenses, and pending payments over a 4–6 week pilot.

Validation methods:

Prototype deployment with 15–25 small businesses

Usage tracking

Feature adoption analysis

Error correction logs

User satisfaction survey

Net Promoter Score

Qualitative feedback

Product-level metrics:

Number of entries recorded per user per week

Percentage of users using the assistant after week 2

Most used features

Number of clarification questions per transaction

Accuracy of classification after user correction

Number of accountant reports generated

Number of pending payment reminders used

3.4 Business Validation

The key business hypothesis is:

The product will be more viable when positioned as a cash-flow visibility and payment control tool for small service businesses rather than as a low-cost bookkeeping assistant for individual freelancers.

Business validation metrics:

Customer Acquisition Cost

Average Revenue Per Account

Gross Margin

Monthly Churn

Customer Lifetime Value

LTV:CAC Ratio

Payback Period

Breakeven Customer Count

Runway

4. Scenario-Based Business Feasibility Model

This section presents a scenario-based model. These figures are illustrative and should be replaced with real data after pilot testing.

4.1 Initial Pricing Model: Low-Cost Individual Plan

Suppose the product is first priced at ₹299 per month for individual small business owners.

A one-month acquisition experiment is conducted through Instagram ads, WhatsApp community promotions, referrals, and founder-led demos.

Assumed acquisition spend: ₹60,000

Sign-ups: 400

Active users: 80

Paying customers: 18

Customer Acquisition Cost:

CAC = Total acquisition spend ÷ Paying customers

CAC = ₹60,000 ÷ 18

CAC = ₹3,333 per customer

At a price of ₹299 per month, the business would require more than 11 months of revenue to recover the acquisition cost before considering operational costs. After accounting for WhatsApp API charges, AI processing costs, customer support, onboarding, failed payments, and churn, the model becomes weak.

This does not mean the product is useless. It means the pricing and target customer segment may not support a sustainable business.

4.2 Revised Business Model: Small Service Business Plan

After analysing user behaviour, the team may discover that the strongest users are not casual freelancers but businesses with multiple clients and recurring payment complexity. These may include wedding photographers, event planners, tutors, interior designers, and boutique service agencies.

The product is repositioned from:

“Simple bookkeeping on WhatsApp”

to:

“Client payment and expense control for small service businesses”

The revised pricing model may include:

Starter Business Plan: ₹1,999 per month

Team Plan: ₹4,999 per month

Assume the ₹1,999 plan has a gross margin of 70%.

Monthly gross profit: ₹1,999 × 70% = ₹1,399

If the CAC is ₹7,000:

Payback Period = CAC ÷ Monthly gross profit

Payback Period = ₹7,000 ÷ ₹1,399

Payback Period = approximately 5 months

For the ₹4,999 team plan, assume a gross margin of 75%.

Monthly gross profit: ₹4,999 × 75% = ₹3,749

If CAC is ₹10,000:

Payback Period = ₹10,000 ÷ ₹3,749

Payback Period = approximately 2.7 months

This model is more attractive because the business can recover acquisition costs faster and has more room to support onboarding, customer service, and product development.

Key Business Insight

The central business insight is that the first product idea may be correct, while the first business model may be incorrect.

The product may be useful to a wide range of users, but not all users are equally valuable from a business perspective. A freelancer who wants occasional expense tracking may appreciate the assistant but may resist paying more than ₹299 per month. A small service business handling multiple clients, advances, pending payments, and vendor bills may experience the same product as a cash-flow control tool and may be willing to pay ₹1,999 or ₹4,999 per month.

Therefore, the stronger business opportunity lies not in generic bookkeeping automation but in financial visibility for small service businesses where missed payments and scattered expense records directly affect cash flow.